The Monetary Policy Committee of the Central Bank of Nigeria will hold its 306th meeting on 20 – 21 July 2026. As in previous meetings, the MPC will review conditions across the parts of the economy that matter for its mandate – real activity, prices, household welfare, the external sector and the fiscal environment – before deciding how to set the policy rate and related instruments.

Under current Nigerian law and the CBN’s evolving inflation‑targeting framework, monetary policy is conducted with price stability as the primary objective, using a limited set of tools centred on the short‑term policy rate. To deploy these tools coherently, MPC members require a continuous, internally consistent view of the real economy:

Is output growing above or below a sustainable pace?

Is inflation genuinely on a disinflation path or showing signs of renewed pressure?

Are household incomes and welfare improving after the recent shock period?

Is the external position (reserves, capital flows, exchange rate) sufficiently robust?

Are upcoming risks broadly balanced, or tilted toward inflation or growth?

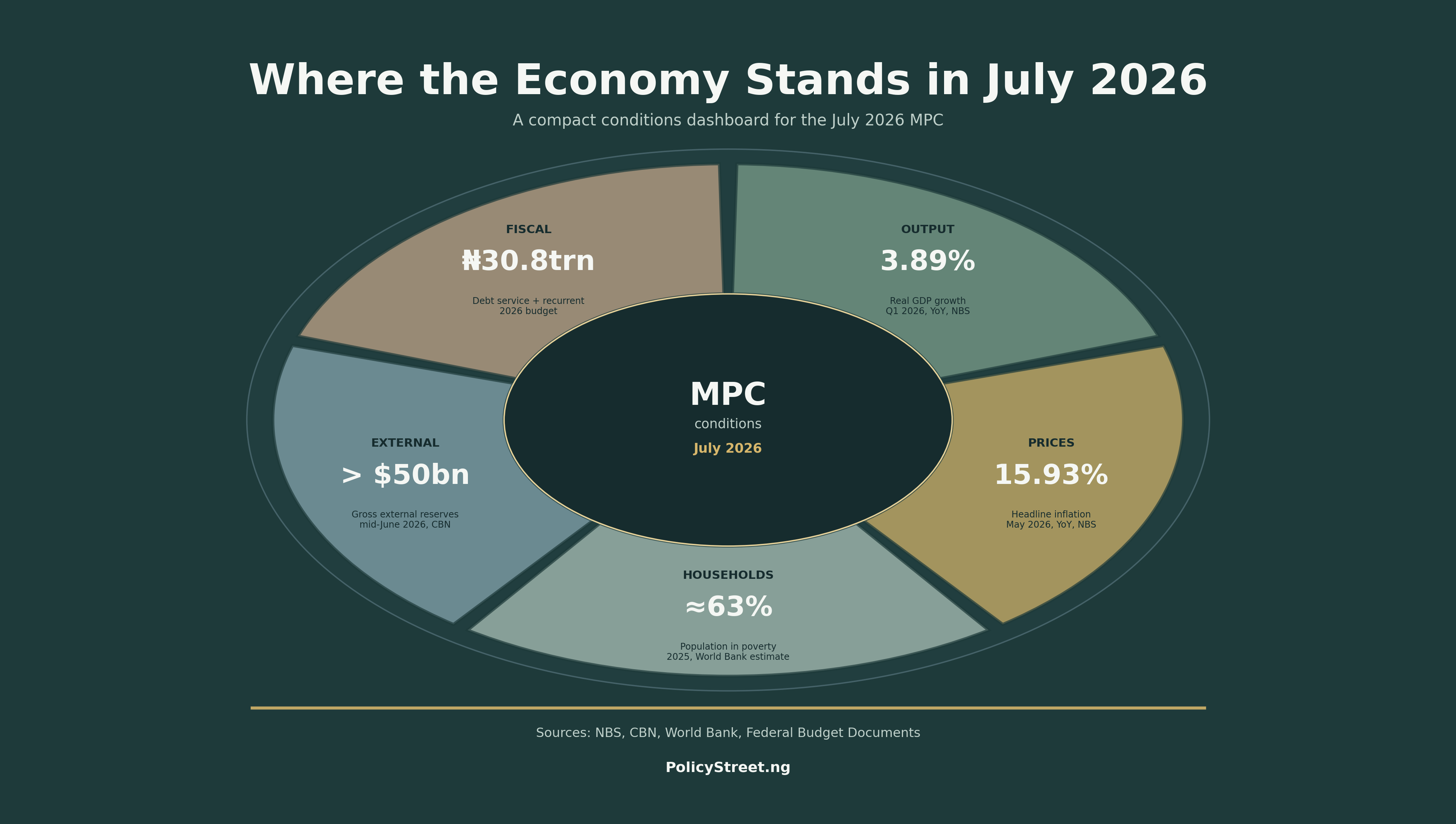

Output: Growth Positive, Momentum Moderating

The National Bureau of Statistics reports that real GDP grew by 3.89 percent year‑on‑year in the first quarter of 2026, higher than the 3.13 percent recorded in Q1 2025 but lower than the 4.07 percent growth in Q4 2025. Services remained the dominant contributor, accounting for 57.73 percent of aggregate GDP in Q1 2026, with agriculture contributing 23.16 percent and industry 19.11 percent.

Sectorally, agriculture expanded by 3.15 percent in real terms in Q1 2026, a marked improvement over the 0.07 percent recorded in the corresponding quarter of 2025. Industry grew by around 3.5 percent, and services by just over 4 percent, indicating broad‑based positive growth.

The data therefore show:

Level: output growth is positive and above the previous year’s Q1 performance.

Direction: quarterly growth has moderated relative to Q4 2025, suggesting some loss of momentum.

From a monetary policy perspective, this is neither a boom nor a contraction. It is a steady, modest expansion whose sustainability depends on price and financial conditions.

Prices: Disinflation Achieved, Then Interrupted

According to the NBS Consumer Price Index report, headline inflation stood at 15.93 percent year‑on‑year in May 2026, up from 15.69 percent in April and 15.09 percent in March – three consecutive monthly increases. The CPI index itself rose from 138.3 in April to 140.7 in May.

Food inflation was 16.96 percent year‑on‑year in May, up from 16.06 percent in April, while core inflation (excluding food and energy) rose to 16.82 percent from 15.86 percent. On a month‑on‑month basis, the headline inflation rate slowed to 1.75 percent in May from 2.13 percent in April, indicating a deceleration in the pace of price increases within the month.

For context, headline inflation in May 2025 was 26.06 percent, and the 12‑month series shows a substantial decline from above 26 percent to just over 15 percent between mid‑2025 and early 2026. The recent data therefore describe:

A successful disinflation phase through 2025.

A subsequent period in 2026 in which the annual rate has turned upward and core pressures are rising, even as monthly momentum has eased.

The IMF’s June 2026 Article IV report attributes much of the renewed inflationary pressure to higher global fuel, food and fertiliser prices linked to the conflict in the Middle East, and recommends that the Central Bank of Nigeria maintain a tight monetary stance with a data‑dependent approach until disinflation is firmly re‑established.

Household Welfare: Gains Have Not Yet Reached Most Nigerians

Macroeconomic aggregates can conceal distributional outcomes. The World Bank’s Nigeria Development Update and related governance diagnostics emphasise that recent reforms have improved macro stability but that conditions for many households remain difficult.

Key points include:

Poverty was estimated at 63 percent in 2025 using the national poverty line, with around 140 million people below that threshold.

Food insecurity affected tens of millions of Nigerians in 2025, driven by high food prices, energy costs and limited social protection.

The World Bank notes that household incomes have not risen sufficiently to offset the earlier period of very high inflation, so the cumulative loss of purchasing power has not been reversed.

From a central bank standpoint, this matters because it shapes the economy’s tolerance for prolonged monetary restriction. Lower current inflation does not restore past real incomes; it merely stops the erosion from accelerating.

External Sector: Stronger Buffers, Higher Dependence on Portfolio Flows

Nigeria’s external position has improved materially. CBN data show gross external reserves rising from $49.80 billion on 1 June 2026 to $50.81 billion by 15 June, crossing and then remaining above the $50 billion mark — the highest level in many years. The increase reflects a combination of current account surpluses, portfolio inflows, Eurobond issuance and FX market reforms.

Capital importation data from the NBS indicate that total capital inflows reached $10.37 billion in Q1 2026, an 83.83 percent increase over the $5.64 billion recorded in Q1 2025 and a 60.97 percent rise compared to Q4 2025. Portfolio investment, particularly in money market instruments and bonds, accounted for the bulk of these inflows.

The implication is straightforward:

External buffers are stronger than at any point in the recent past.

That strength is significantly supported by interest‑sensitive portfolio flows, which are themselves influenced by the level of domestic rates and perceptions of policy credibility.

For monetary policy, this creates a linkage: rate decisions affect not only domestic borrowing conditions but also the composition and stability of external financing.

Fiscal Environment: Improved Revenue, Persistent Structural Pressures

On the fiscal side, a separate set of official documents – the 2026 Appropriation Act and associated budget framework – shows that the federal government’s expenditure profile is still heavily weighted toward debt service and recurrent spending. The IMF’s Article IV report notes that interest payments as a share of federal revenue remain high, and calls for continued efforts to strengthen public financial management and avoid off‑budget commitments.

The same report emphasises that recent revenue mobilisation, subsidy reform and FX market changes have improved fiscal sustainability, but warns that expanded spending pressures, especially around elections, could complicate the disinflation process if not managed within a consistent framework.

From the MPC’s perspective, the fiscal environment is therefore characterised by:

More robust revenues and some consolidation.

Ongoing structural pressures from debt service and recurrent obligations.

The risk that pre‑election spending could offset monetary efforts to contain inflation.

Summary

Taken together, current data portray an economy in modest expansion, with disinflation partly achieved but not yet secure, household welfare still under strain, and an external position strengthened by reforms and high interest‑sensitive inflows. The July MPC is therefore not choosing between “high” and “low” rates in the abstract, but between protecting price and exchange‑rate stability on the one hand and easing tight financial conditions on the other, in a setting where no single decision can fully satisfy both macroeconomic and welfare objectives.

Reference

National Bureau of Statistics (2026) Gross Domestic Product (GDP) Q1 2026 Report. Available at: https://www.nigerianstat.gov.ng

Central Bank of Nigeria (2026) Monetary Policy Committee decisions and calendar. Available at: https://www.cbn.gov.ng

International Monetary Fund (2026) Nigeria: 2026 Article IV Consultation – Staff Report. Available at: https://www.imf.org

World Bank (2026) Nigeria Development Update. Available at: https://www.worldbank.org

Federal Government of Nigeria (2025) Appropriation Act 2026 and Fiscal Framework. Available at: https://budgetoffice.gov.ng