When Nigeria's Central Bank raises its interest rate, commercial banks raise the rates they charge borrowers quickly and by a large amount. When the Central Bank cuts its rate, commercial banks reduce what they charge borrowers slowly and by a small amount. The International Monetary Fund documented this pattern in a detailed study published in June 2026, and the numbers are significant enough to warrant serious examination.

How interest rate transmission works

The Central Bank of Nigeria – the CBN – sets a benchmark interest rate called the Monetary Policy Rate. This rate signals the price of money in the economy. When the CBN raises it, borrowing becomes more expensive and the economy tends to slow. When the CBN cuts it, borrowing becomes cheaper and the economy tends to expand.

This mechanism only functions as intended if commercial banks pass the change on to their customers. A one percentage point increase in the CBN rate should, in a well-functioning market, produce roughly a one percentage point increase in the rates banks charge businesses and households for loans. The same applies in reverse when the CBN cuts.

One basis point is one-hundredth of one percentage point. The IMF study measures transmission in these units, because the differences between what the CBN moves and what banks pass on are large enough that imprecise language would obscure the scale of the problem.

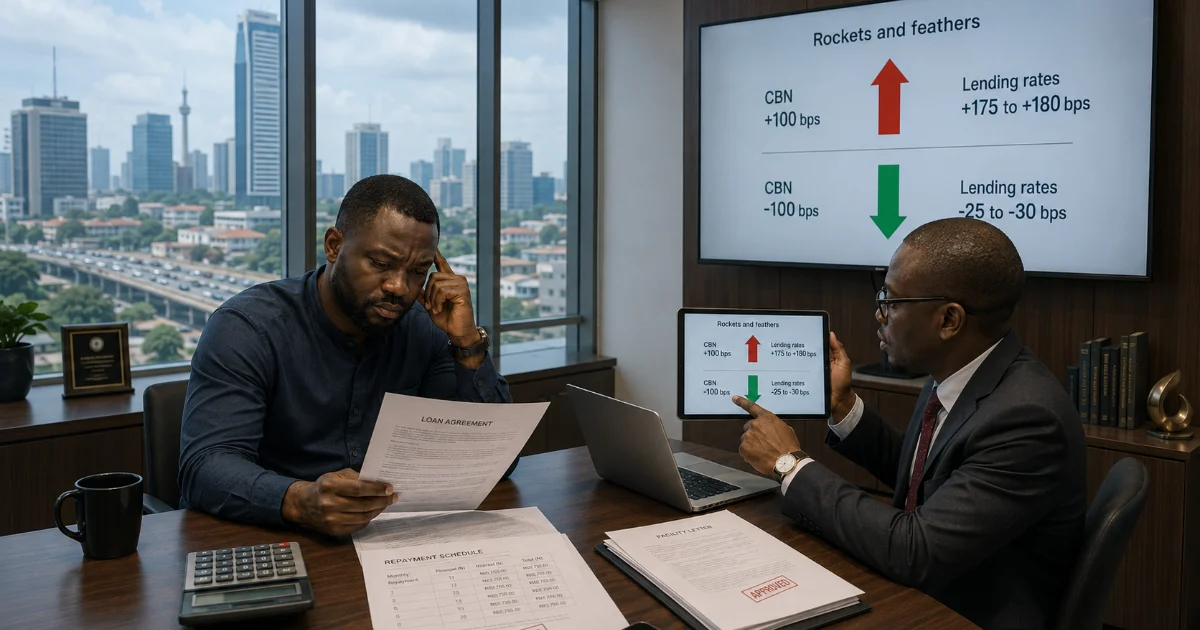

What the IMF found

According to the IMF's June 2026 Selected Issues Paper on Nigeria, when the CBN raises its rate by 100 basis points – one full percentage point – commercial banks raise their lending rates by 175 to 180 basis points. When the CBN cuts its rate by 100 basis points, commercial banks reduce their lending rates by only 25 to 30 basis points.

The asymmetry is substantial. On the tightening side, banks amplify the CBN's move by roughly 75 percent. On the easing side, banks absorb roughly 75 percent of the cut rather than passing it to borrowers.

Why this happens

Two forces explain the pattern, and both matter.

The first is market structure. Nigeria's five largest commercial banks – Access, UBA, Zenith, First HoldCo, and GTCO – collectively hold more than three-quarters of the banking industry's total assets, which stood at ₦161.3 trillion at the end of 2025. In a market this concentrated, banks do not face strong competitive pressure to pass rate reductions on to borrowers. If all major banks hold lending rates at a similar level, no individual bank loses customers by doing the same. A more fragmented, competitive market would erode this behaviour, because a bank offering cheaper loans would attract borrowers away from those that do not.

The second force is rational caution about risk. When the CBN raises rates, borrower default risk rises alongside funding costs. Banks raise lending rates partly because they are repricing genuine risk, not solely to protect profit. When the CBN cuts rates, banks are not always certain the easing will persist – particularly in an economy with a history of inflation volatility. Cutting lending rates prematurely, only to have the CBN tighten again months later, creates its own problems. Some degree of caution on the easing side reflects prudent risk management rather than purely opportunistic behaviour.

Both forces are probably operating simultaneously. The IMF study identifies the asymmetry clearly; it is less definitive about the precise contribution of each cause.

The cumulative effect on borrowers

Over a complete monetary policy cycle – rates rise by one percentage point, then fall by the same amount – a borrower should end up roughly where they started. Under Nigeria's current transmission pattern, they do not.

On the way up, the lending rate increases by approximately 1.75 to 1.80 percentage points. On the way down, it decreases by approximately 0.25 to 0.30 percentage points. The net effect after a full cycle is a structural increase in the cost of credit of roughly 1.5 percentage points above the starting level. Over multiple policy cycles across several years, this compounds. Businesses and households face a structurally higher cost of borrowing than the CBN's official rate would suggest, not because the CBN set rates higher, but because the transmission mechanism distributes the burden unevenly.

What this means for monetary policy

The CBN's primary tool for managing the economy is the Monetary Policy Rate. If transmission is asymmetric, that tool works differently in each direction.

During tightening, the CBN raises rates to reduce inflation by slowing credit growth and economic activity. Asymmetric transmission amplifies this effect – businesses face sharper credit cost increases than the CBN rate alone implies. The policy works, but with more force than intended.

During easing, the CBN cuts rates to stimulate credit and investment. Asymmetric transmission weakens this effect – borrowers receive only a fraction of the intended relief, credit conditions loosen modestly, and the stimulus does not reach the real economy at the scale the policy rate change would suggest.

The implication is not that CBN policy is ineffective, but that its effects are unevenly distributed across the cycle. Tightening bites harder than prescribed. Easing stimulates less than intended.

What the CBN could do

The IMF study does not prescribe a specific remedy, but several options follow logically from the diagnosis.

Transparency requirements would require banks to publish their pass-through rates – the percentage of each CBN rate change they transmit to lending rates – on a regular, public basis. This creates reputational accountability without direct price regulation. Banks that consistently under-transmit cuts would face scrutiny from borrowers, investors and the regulator.

Competition policy could reduce the barriers that prevent new banks and financial technology lenders from entering the credit market at scale. Greater competition would erode the market structure that currently allows banks to retain much of the benefit of rate cuts. The IMF identifies this as the most structurally durable solution.

The CBN could also adjust the size of its rate changes to account for known transmission asymmetries – cutting more aggressively during easing cycles to produce the borrower-level relief the policy is designed to deliver. This is technically feasible and does not require regulatory intervention in bank pricing.

Conclusion

It would be inaccurate to characterise Nigerian banks as simply extracting rent from borrowers. Some portion of the asymmetry reflects genuine risk repricing during tightening cycles and rational caution during easing. Banks operate in an economy where inflation has been volatile and policy reversals have occurred, and their pricing behaviour partially reflects that environment.

At the same time, the scale of the asymmetry – 175 basis points on the way up against 25 on the way down – exceeds what risk adjustment alone would justify. The market structure findings are consistent with the interpretation that concentration plays a significant role in allowing banks to retain a disproportionate share of the benefit when rates fall.

The consequence for the broader economy is real: businesses and households pay more for credit than the CBN's policy rate would imply, monetary easing transmits weakly to investment and consumption, and each tightening cycle leaves a residue of higher credit costs that easing does not fully reverse.

Sources: IMF Selected Issues Paper, Nigeria, June 2026; Nairametrics, June 2026; The Nation, May 2026; NGX and Nairalytics deposit data, H1 2025.